Overview

This document defines the intraday trading strategy used to benchmark Quantum Signals' direction-to-close predictions. The strategy is intentionally simple: it converts each signal update into a fixed-size trade, accumulating position over the session in the direction the signal indicates.

Core idea: Divide the daily portfolio into equal-sized units. Every 5 minutes, read the signal. If UP, buy one unit. If DOWN, sell one unit. If STABLE, do nothing. Close everything at end of day.

How to use this strategy: Follow it exactly as presented to replicate our published benchmark results. Beyond that, customers typically either combine the signal with other signals or strategies in an ensemble, or improve on this baseline by adding leverage, stop-losses, position limits, or other risk management rules suited to their portfolio.

1. Signal Direction Convention

The signal predicts whether the current price will rise or fall toward the session close:

| Signal | Meaning |

|---|---|

| UP | Current price is below the session close → price will rise toward close |

| DOWN | Current price is above the session close → price will fall toward close |

| STABLE | No directional conviction |

2. Setup

Trading window

| Phase | Time |

|---|---|

| Opening positions | 09:45 – 15:30 ET (every 5 minutes, 70 decision points) |

| Exiting positions | 15:55 – 15:59 ET (close all remaining positions) |

Decision interval

The default decision interval is 5 minutes, but the strategy generalizes to other intervals. Using 10-minute, 20-minute, or 30-minute decision intervals produces similar results — the position size unit S adjusts proportionally, and the decision logic is identical. The 5-minute interval is used here because it matches the granularity at which we publish benchmark results.

Position size unit (S)

The strategy divides the daily notional equally across all decision points:

S = Daily Notional ÷ (Price × Number of Decision Points)

Rounded to the nearest whole number. Each decision point trades exactly S units.

Example — S&P 500:

- Daily notional: $500,000

- S&P 500 price: ~$7,000

- S = round(500,000 ÷ 7,000 ÷ 70) = round(1.02) = 1 unit per decision point

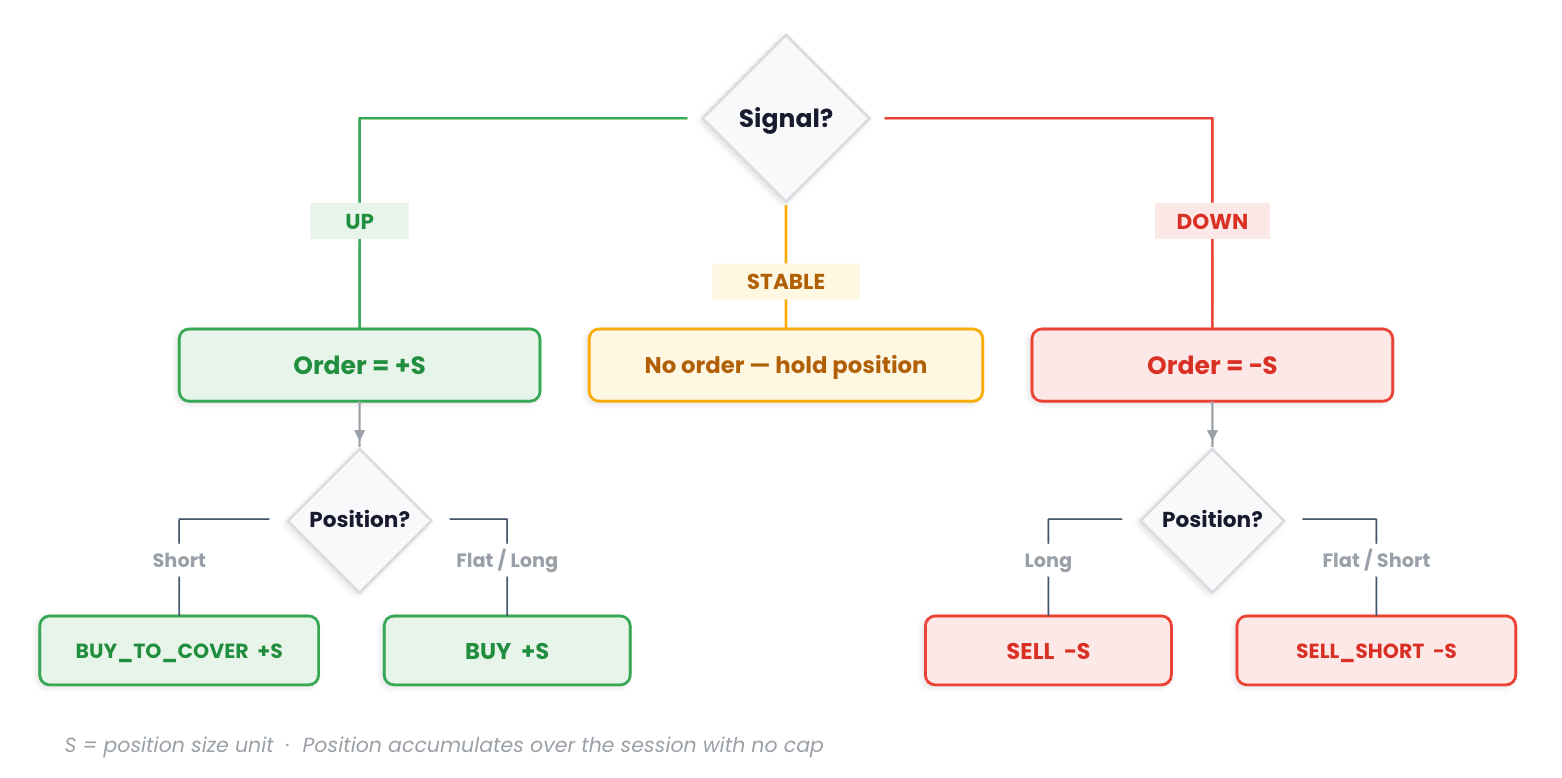

3. Decision Logic

At each 5-minute decision point, read the signal and determine the order:

The net position accumulates over the session. There is no position cap — if the signal stays UP for 20 consecutive decision points, the position reaches Long 20S.

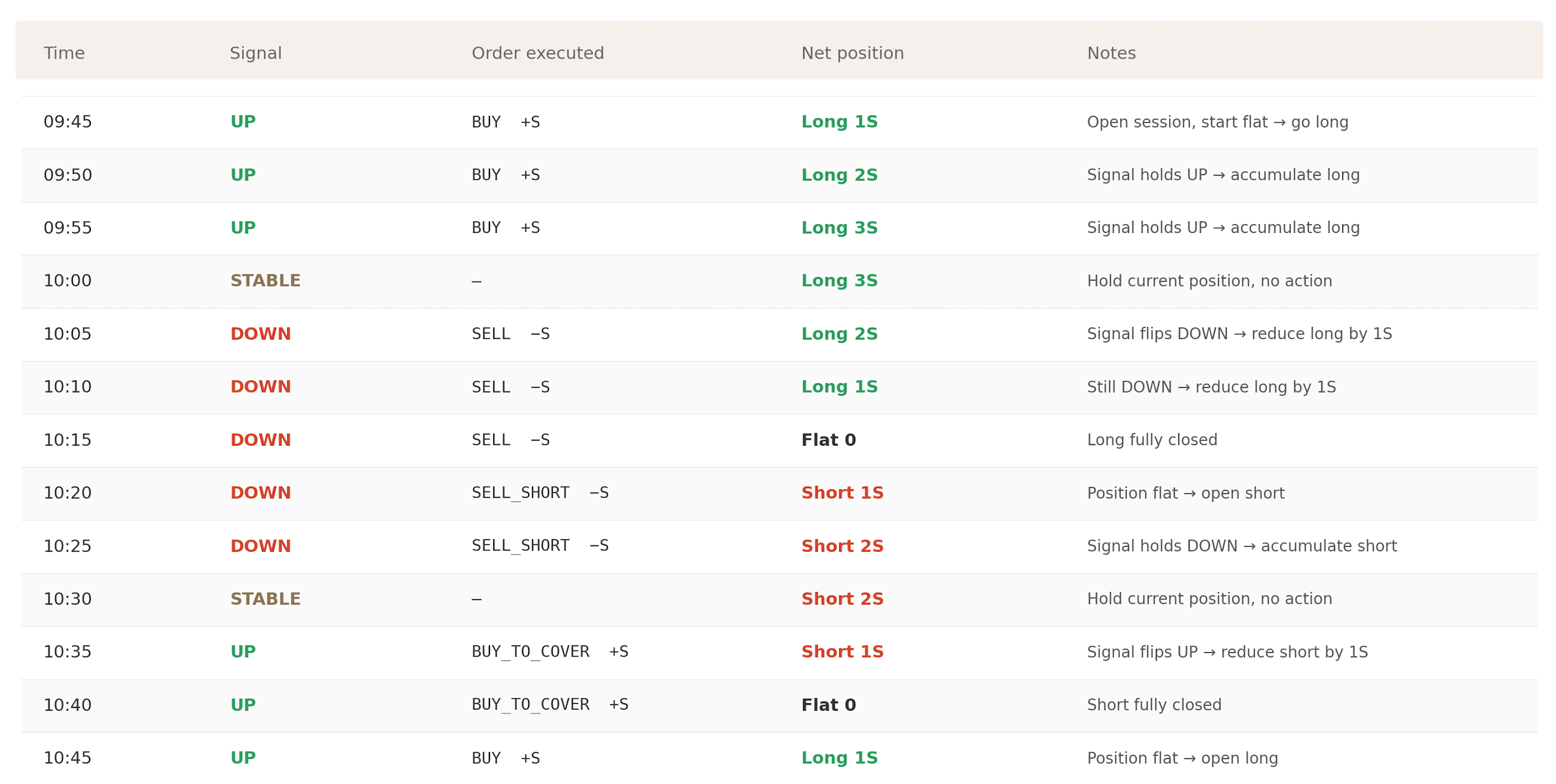

4. Example

The table below shows the first hour of a session. The strategy starts flat and accumulates position as the signal changes direction.

S = position size unit (1/70 of daily portfolio). Signal cadence: every 5 min shown here; live signal updates every 1 min.

Key observations:

- When the signal flips direction, the strategy first unwinds the existing position before building in the new direction. It does not jump from Long 3S to Short 1S in a single step — it sells down one unit at a time.

- STABLE signals are a pause. No trading occurs, and the position is unchanged.

- The order type (BUY vs. BUY_TO_COVER, SELL vs. SELL_SHORT) is determined by the current position, not the signal itself. The signal only determines direction (+S or −S).

5. End-of-Day Close

The last signal is read and traded at 15:30 ET. At 15:31 ET, the strategy stops reading signals. No trades are executed between 15:31 and 15:54 — the position is held as-is.

At 15:55 ET, the strategy begins exiting the current position. All remaining positions are closed by 15:59 ET to ensure the strategy is flat at session close.

If the position at 15:55 is Long 5S, the strategy sells 5S over the final 4 minutes. If Short 3S, it buys to cover 3S.

6. What This Strategy Does NOT Do

- No leverage. Position size is derived from a fixed daily notional divided across all decision points.

- No position limits or risk gates. The position accumulates freely based on signal direction.

- No intra-interval order splitting. Each decision point executes S units as a single order at the decision time. There is no spreading across the minutes within a 5-minute interval.

- No sizing. Every decision point trades the same size S, regardless of signal history or market conditions.

- No overnight positions. Everything is closed by 15:59 ET.